We are proud to publish our catalogue for 2023. Download the full catalogue here. Visit our website, www.thebehaviourshop.com for further information, as well as to access our social media.

We are proud to publish our catalogue for 2023. Download the full catalogue here. Visit our website, www.thebehaviourshop.com for further information, as well as to access our social media.

AssessmentWorld Pty Ltd suggests an alternative approach to human capital measurement and reporting (read the full article at: https://bit.ly/3d50691 ). This approach is built on a philosophy of measuring for the sake of managing, versus measuring for the sake of reporting. This means that the focus of the measurements is to internally improve on the employment of human capital over time, and to track and measure said. This approach differs fundamentally from one where measuring is done against the myriad of metrics that exist, with the view to comply with external indicators, standards and disclosures. Human capital measurement is a highly fragmented area of management practice, and we posit that the current reporting in integrated statements, reflects the same condition.

AssessmentWorld Pty Ltd also of the view that efforts to standardise HC measurement, for the sake of ‘coherent’ reporting and comparability, will be an exercise in futility, as, for one, organisations differ substantially in the way they operate in a specific time span. A quantitative example would be the differences between organisations on a metric such as labour costs as a percentage of revenue (LCPR). Company A might reflect a LCPR of 50%, and an EBITA of 12%, versus Company B, reflecting a LCPR of 20%, and an EBITA of 3%. Clearly the LCPR metric in this example could be interpreted incorrectly, if simply read on its own.

A qualitative measurement example would be the differences between companies on a metric such as a Staff Satisfaction Index (SSI), using a Likert scale. Company A might score a Sten 8 on an SSI instrument, indicating a high SSI, versus Company B, scoring a 6, i.e. average SSI. Deeper understanding of the workings of the two companies during the reporting period, reveals that Company B changed executive leadership, and was driving an aggressive growth strategy, demanding greater levels of input and quality from employees. The mere Sten score on the SSI does not explain the more complex and stressful interactions in Company B during that period, versus Company A, which, during the same period, was experiencing exponential market growth, offering its employees expansive bonuses.

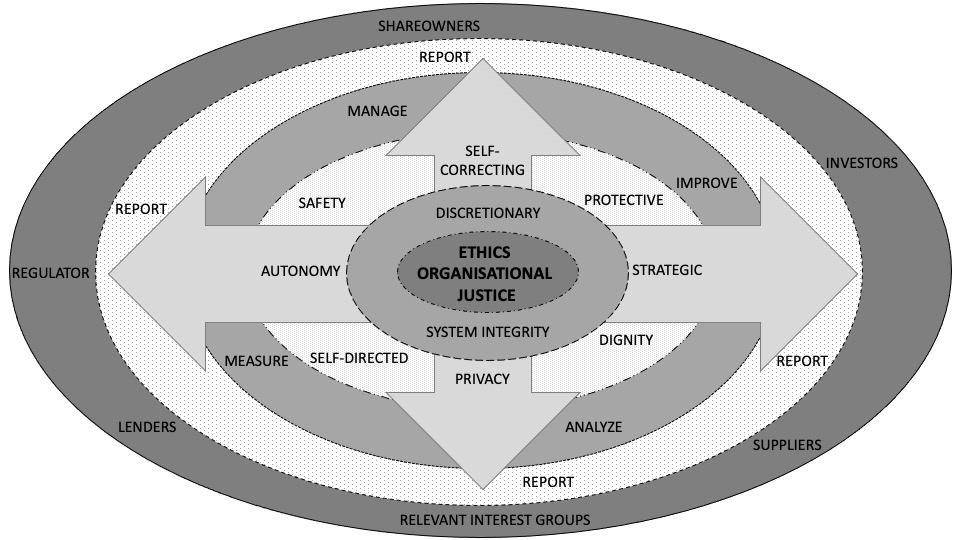

AssessmentWorld Pty Ltd suggests an Intra-systemic HC Measurement Model for the use of HC measurements in organisations:

• HC measurement and management should be based on ethical principles, such as fairness, honesty, loyalty, care, accountability, and responsibility.

• Based on ethics and organisational justice, managers should execute HC measurement and management, discretionary, whilst ensuring system integrity.

• Discretionary system integrity, now enables managers to create privacy, dignity, safety and protection, both physically and psychologically for the organisation’s human capital. It also enables management to self-direct human capital autonomously and strategically, and to self-correct, where indicated by measures.

• It then follows that managers have the autonomy to measure, analyse, improve and manage human capital from a quality management perspective, i.e. deriving the highest levels of returns on human capital, be it quantitatively or qualitatively measured.

• Measurement, analysis, improvement and management of human capital, as described above, is a continuous process, therefore, when integrated reporting for stakeholders is done, it should report on this process via uncomplicated, concise and informative narratives. These narratives should be integrative in nature, without unrelated, complicated quantifications and data representations. In short, the ‘story’ of how human capital was deployed in a particular year, should be presented.

The implementation of the Intra-systemic HC Measurement Model creates various implications for organisational managers in order to give effect to its principles and execution:

• Management in this context refers to all line managers in the organisation, and not just HR management. The latter has to indeed take the lead here, as human capital measurement-management is their specialist area. All organisational managers, however, have to be trained and skilled in these areas, as they mostly engage with employees during performance within the operations of the organisation.

• Determination has to be made regarding what is material and important for the organisation to measure in terms of its human capital efficiencies. A combination of quantitative and qualitative measures may be decided upon.

• Managers also need to be clear as to how, and with what they want to measure. This would include, how often these measures need to be applied, and would depend on organisational specific needs. Instruments, such as, accounting, production and HR data, surveys, and performance appraisal outcomes are some of the measures which can be used.

• A vital component of model execution, is the decision/s as to how to translate the measures into human capital efficiency improvements. Management by objectives (MBO) comes to mind here, with clearly defined key performance areas and indicators, linked to clear time lines.

• Change management is a competency that needs to be employed, to ensure buy-in, motivation and engagement. Employees who are made to feel important as human capital, and not mere labour, will be less resistant and more inclined to partake in improvements, such as upskilling, adapt to new work flows, and the like.

• General managerial actions, such as controlling, monitoring, and remediation, should be applied. Managerial agility would lead to timely identification of deviations, and implementation of corrective actions.

• Continuous measurements of improvements should be documented and communicated internally, as this leads to further re-enforcement of efficiency changes implemented.

• At the end of a financial year, organisations will then possess of rich sets of data to narrate to external stakeholders in an integrated manner, using a mix of quantitative and qualitative data. The organisation now tells its human capital measurement and management story, which is unique to its identity and circumstances.

Within the Intra-systemic HC Measurement Model approach, standard developers and regulators need to take note of the following implications:

• The idea of developing and prescribing a plethora of standards and regulations, purely for the sake of reporting, will be counter-productive. Measuring for the sake of managing is rather the philosophy to be introduced here.

• Specific standards and regulations should be non-negotiable and enforceable, such as, physical and psychological health and safety, rights of employees, workplace ethics, including non-discriminatory management, and the like.

• Most standards should, however, be voluntary, enabling organisations to move freely, and narrate their unique human capital efficiency improvement ‘story’ on their own terms, utilising these voluntary standards as guidance and framework.

• A mix of quantitative and qualitative standards and regulations should be developed and made available, in order to assist organisations to choose those who most aptly apply to them and their specific circumstance at a specific time. This will afford organisations the capability to develop integrated narratives regarding their human capital within a broad, mostly voluntary framework of standards. The approach should also allow all stakeholders to make an informed assessment as to the truthfulness and trustworthiness of said narratives, as well as enable comparability within and across industries, and over various time frames.